Introduction to Options

Options Basics

Definition

Options are

-

A form of derivative financial instrument

-

Two parties contractually agree to transact an asset at a specified price before a future date.

An option gives its owner the right to either buy or sell an asset at the exercise price.

The owner is NOT obligated to exercise the option.

:orange_book: When an option reaches its expiration date without being exercised, it is rendered useless with no value.

Derivatives

Options are derivatives of financial securities – they derive their value from an underlying asset.

Other examples of derivatives

- Forwards and Futures

- Warrants

- Swaps

Etc.

Quote Details

-

Volume (VLM) – how many contracts of a particular option were traded during the latest session.

-

The bid price – is the latest price at which a market participant wishes to buy a particular option.

-

The ask price – is the latest price offered by a market participant to sell a particular option.

-

The strike price – is the price at which the buyer can buy or sell the underlying security if they choose to exercise the option.

-

Expiration date – This is when an option expires and becomes worthless.

-

Option premium – is the price at which an option is purchased.

-

Open Interest – shows the number of contracts in existence for the option. This figure is only updated once a day and will differ from volume. At the end of the trading day, all contracts that were closed are subtracted from open interest and all contracts that were open are added to open interest.

-

Adjusted Options – Sometimes, an option will be displayed on the chain with an “A”. This is calling out that an adjusted option exists within the options series. You may notice an adjusted option has different volume and quotes displayed.

-

Last – The last price represents the last price at which the option was traded. This could be an opening or a closing transaction. It is important to note that the last time an option was traded could be within seconds, minutes, days, weeks, or even months and may not be an accurate depiction of the current value of the option.

The last price in conjunction with the bid and ask is used to quote the value of the option. -

Change – The change displays the difference between the last price and the previous day’s close.

Trading Platform

Option contracts are traded either on

- a public stock exchange (also known as the ETO (Exchange Traded Options)), or

- OTC – Over The Counter

Parties

Buy / Sell

Options Holders – People who buy options

Options Writers – People who sell options

Buyers

-

not obligated to buy or sell

-

Have the choice to exercise their rights

-

This limits the risk of buyers of options to only the premium spent

Sellers

-

obligated to buy or sell if the option expires in the money.

-

may be required to make good on a promise to buy or sell

-

have exposure to more – and in some cases, unlimited – risks

-

can lose much more than the price of the options premium

Risk Neutrality

Option pricing assumption: Risk neutrality – investors are not risk-averse nor risk-seeking

Buyers vs Sellers

| Option | Buyer’s Right | Seller’s Obligation | Seller’s Right |

|---|---|---|---|

| Call options | Buy the underlying stocks from the seller at a specific price on or before the expiration dates | Sell the underlying stocks to the buyer at the strike price on or before the expiration of the option | Keep the premium |

| Put options | Sell the underlying stocks to the options seller at a specific price on or before the expiration dates | Buy the underlying stocks from the buyer of the option at the strike price on or before the expiration of the option | Keep the premium |

Usage

Options are used on

- Individual stocks

- Exchange-traded funds (ETFs) – a type of pooled investment security similar to a mutual fund

- Currencies

- Stock market indexes

- Bonds

etc.

Benefits

Options are powerful because they can enhance an individual’s portfolio by adding

- income

- protection

- hedge

- leverage

- speculation

etc

Example – We can use options as an effective hedge against a declining stock market to limit downside losses.

Financial Story

For example, 🍎 If you are a farmer and you grow apples in spring.

You worry that the apples’ price will drop in autumn. Then you can pay a premium and agree with the acquirer that you have the right to sell the apple at £1/kg.

In the autumn

- if the market price is £0.5/kg, you can execute the option and sell the apples at £1/kg.

- if the market price is £1.5/kg, you can ignore the contract and sell it in the market.

![]()

Options Arbitrage

Options arbitrage trades are commonly performed in the options market to earn small profits with very little or zero risk.

Traders perform conversions when options are relatively overpriced by purchasing stock and selling the equivalent options position.

Traders will do reverse conversions or reversals when the options are relatively underpriced.

In practice, actionable option arbitrage opportunities have decreased with the advent of automated trading strategies.

Options vs Other Financial Products

Stock vs. Options

Similarities

- Listed options are securities like stocks

- Options trade like stocks

- Options are actively traded in a listed market like stocks

Differences

- Options are derivates, unlike stocks

- Options have expiration dates, while stocks do not

- There is not a fixed number of options, as there are with stock shares available

- Stock owners have a share of the company with voting and dividend rights, unlike options

Option vs Future

| Futures | Options |

|---|---|

| Futures is a pure trading tool | Options is a risk-limiting tool |

| Both parties share the risk | Risk is mostly taken by the seller |

| Futures can be bought and sold in the derivatives market | Options can also be bought and sold in the derivatives market |

| The amount of loss or profit that one can make in a futures contract depends on the price at the time of execution of the contract | The amount of loss is restricted to the option premium paid. |

Exiting the Options

Once you own an option, you can use three methods to make a profit or avoid loss:

- exercise it

- offset it with another option

- let it expire worthless.

In practice,

10% of options are exercised

30% expire worthlessly

60% are traded (closed) out

Exercise

Use the right to buy or sell the underlying security specified in the options contract.

As the holder of the call option, you can exercise your right to buy throughout the life of the option up to your brokerage firm’s exercise cut-off time on the last trading day.

Offsetting

An offset involves assuming an opposite position of an original opening position in the securities markets.

For example, if you are long 100 shares of XYZ, selling 100 shares of XYZ would be the offsetting position. Traders can also generate an offsetting position through hedging instruments, such as futures or options.

i.e.

You must sell the call with the same strike price and expiration if you bought a call. You must buy a call with the same strike price and expiration if you sell a call. You must sell a put with the same strike price and expiration if you bought a put. You must buy a put with the same strike price and expiration if you sell a put. If you do not offset your position, you have not officially exited the trade.

Expiry

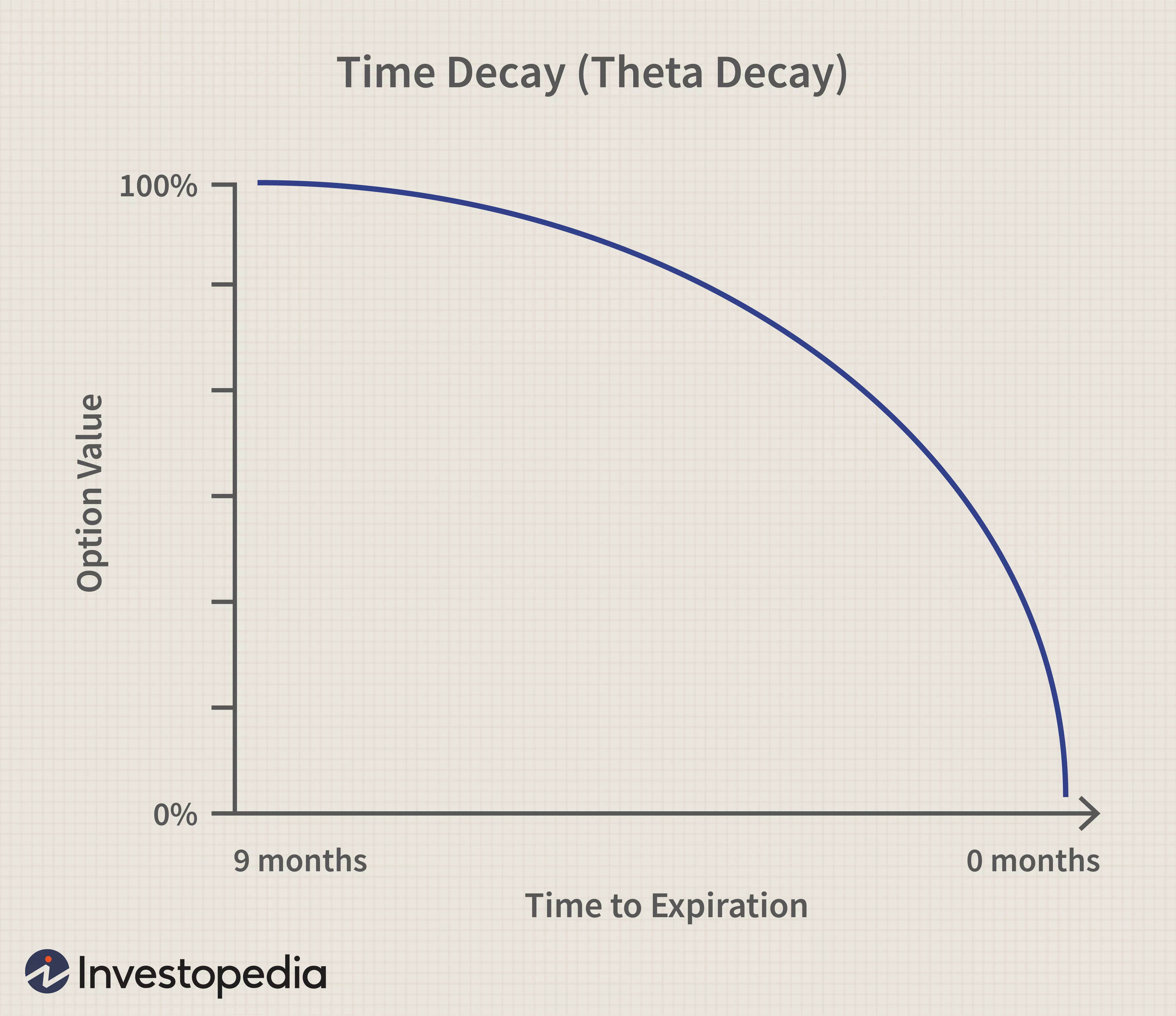

Time works against us if we have options

-

its time value decays as the time goes by

-

value is 0 once expired

Time value – the amount an investor is willing to pay for an option above its intrinsic value.

This amount reflects the hope that the option’s value increases before expiration due to a favourable price change in the underlying security.

image source: https://www.investopedia.com/terms/t/timedecay.asp

Strike Price

A strike price is a set price at which a derivative contract can be bought or sold when exercised.

For call options, the strike price is where the option holder can buy the security; for put options, the strike price is the price at which traders can sell the security.

-

The strike price is also known as the exercise price.

-

The value of a derivative is based on its underlying asset.

Call / Put

Call

It gives the call option buyer the right, but not the obligation, to buy the financial instrument at a specific price – the strike price of the option – within a specified time frame.

The seller of the option is obligated to sell the security to the buyer if the latter decides to exercise their option to make a purchase.

The buyer can exercise the option before the specified expiration date—the expiration date may be three months, six months, or even one year in the future.

Put

A put option is an option contract that gives the buyer the right, but not the obligation, to sell the underlying security at a specified price (also known as the strike price) before or at predetermined expiration date.

They protect against the decline in the price of such assets below a specific price.

(Profit and Loss) P & L Table

| Underlying Asset Big Fall | Underlying Asset Small Fall | Sideways | Underlying Asset Small Rise | Underlying Asset Big Rise | |

|---|---|---|---|---|---|

| Buy Call | Loss | Loss | Loss | Loss or Profit | Big Profit |

| Sell Call | Profit | Profit | Profit | Profit or Loss | Big Loss |

| Buy Put | Big Profit | Profit or Loss | Loss | Loss | Loss |

| Sell Put | Big Loss | Loss or Profit | Profit | Profit | Profit |

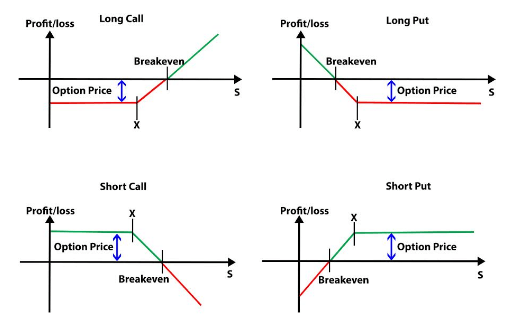

Trading

There are four things we can do with options:

- Buy (long) calls

- Sell (short) calls

- Buy (long) puts

- Sell (short) puts

image source: https://static.seekingalpha.com

Max Gain / Loss

| Maximum Gain | Maximum Loss | |

|---|---|---|

| Call Buyer | Unlimited | Premium |

| Put Buyer | Limited | Premium |

Call Options vs . Put Options

| Call Options | Put Options |

|---|---|

| Used to hedge against traders’ position of a declining price for the security or commodity. | Used to hedge against traders’ position of a rising price for the security or commodity. |

| Holders of American depository receipts (ADRs) in foreign companies can use call options on the U.S. dollar to hedge against declining dividend payments. | Manufacturers in foreign countries can use their native currency for payment. |

| Short sellers use call options to hedge against their positions. | Short sellers have limited gains from put options because a stock’s price can never fall below zero. |

Option Catagories

American-Style vs European-Style

American-style exercise – you can exercise your contract any day the market is open before the expiration date. The last day to exercise a monthly American-style option is usually the third Friday of the month when the contract expires (expiration Friday).

Most, but not all, index options use European-style exercise – you can exercise your contract is the last trading day (usually Friday) before expiration.

Even though there is only one day to exercise your contract, you can always close out your option position in the market any day before expiration.

Naked Options vs Covered Options

Naked – A call (or put) written without the offsetting shares (or funds) necessary to fulfil the terms of the contract should it be exercised by its buyer.

Suppose a seller writes an uncovered options contract. In that case, they assume the contract will not move into the money and be exercised by its buyer.

Exotic Option vs. Traditional Option

Exotic options are a category of options contracts that differ from traditional options in their payment structures, expiration dates, and strike prices.

The underlying asset or security can vary with exotic options allowing for more investment alternatives. Exotic options are hybrid securities often customisable to the investor’s needs.

Exotic options can be customised to meet the investor’s risk tolerance and desired profit.

Although exotic options provide flexibility, they do not guarantee profits.

Short-Term Options Vs. Long-Term Options Vs. Long-Term Equity Anticipation Securities (LEAPs)

Short-term options are those that generally expire within a year. Long-term options with expirations greater than a year are classified as long-term equity anticipation securities (LEAPs). LEAPs are identical to standard options except that they have longer durations.

| Short-Term Options | Long-Term Options | LEAPs |

|---|---|---|

| Time and extrinsic value of short-term options decay rapidly due to their short durations. | Time value does not decay as rapidly for long-term options because they have a longer duration. | Time value decay is minimal for a relatively long period because the expiration date is a long time away. |

| The main risk component in holding short-term options is the short duration. | The main component of holding long-term options is using leverage to magnify losses to conduct the trade. | The main risk component in holding LEAPs is an inaccurate assessment of a stock’s future value. |

| They are fairly cheap to purchase. | They are more expensive compared to short-term options. | They are generally underpriced because it is difficult to estimate stock performance far out in the future. |

| They are generally used during catalyst events for the underlying stock’s price, such as an earnings announcement or a major news development. | They are generally used as a proxy for holding shares in a company and with an eye toward an expiration date. | LEAPs expire in January, and investors purchase them to hedge long-term positions in a given security. |

| They can be American- or European-style options. | They can be American- or European-style options. | They are American-style options only. |

| They are taxed at a short-term capital gains rate. | They are taxed at a long-term capital gains rate. | They are taxed at a long-term capital gains rate. |

Premium

Definition

An option premium is the current market price of an option contract. It is thus the income the seller (writer) receives from an options contract to another party.

Premium Valuation is essentially all about determining the probabilities of future price events.

Premium = \text{Intrinsic Value} + \text{Time Value}

For stock options, the premium is quoted as a dollar amount per share, and most contracts represent the commitment of 100 shares.

Example

| May 1 | May 21 | Expiry Date | |

|---|---|---|---|

| Stock Price | $67 | $78 | $62 |

| Option Price | $3.15 | $8.25 | worthless |

| Contract Value | $315 | $825 | $0 |

| Paper Gain/Loss | $0 | $510 | -$315 |

then the premium is

| Premium = | Intrinsic Value + | Time Value |

|---|---|---|

| $8.25 | $8.00 | $0.25 |

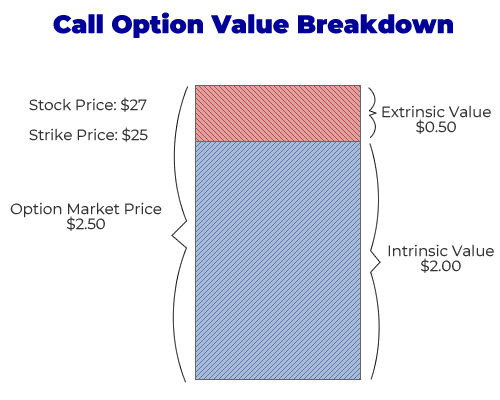

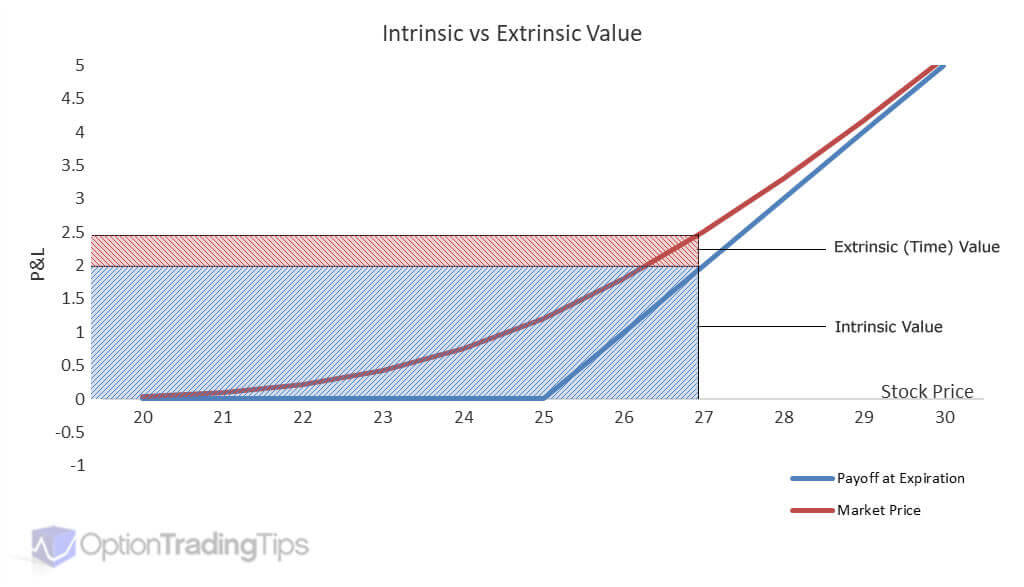

Intrinsic and Extrinsic/Time Value

Intrinsic Value (Calls)

A call option is in-the-money when the underlying security’s price is higher than the strike price.

\begin{gathered}\text { Intrinsic Value } \\ (\text { Calls })\end{gathered} \quad=\quad \begin{gathered}\text { Current Price }\end{gathered} \quad - \text { Strike Price }

Intrinsic Value (Puts)

A put option is in-the-money if the underlying security’s price is less than the strike price.

\begin{gathered}\text { Intrinsic Value } \\(\text { Puts})\end{gathered} \quad= \text { Strike Price } - \text {Current Price }

Extrinsic/Time Value

Time value is any premium above intrinsic value before expiration.

Time value is often explained as the amount an investor is willing to pay for an option above its intrinsic value.

This amount reflects the hope that the option’s value increases before expiration due to a favourable price change in the underlying security.

Because time is a component of the price of an option, a one-month option will be less valuable than a three-month option. This is because with more time available, the probability of a price move in your favour increases, and vice versa.

Accordingly, the same option strike that expires in a year will cost more than the same strike for one month. This wasting feature of options is a result of time decay. The same option will be worth less tomorrow than today’s if the stock price doesn’t move.

Image source: https://www.optiontradingtips.com/images/option-value-breakdown.png

Black-Scholes Model

Black-Scholes is a pricing model used to determine the fair price or theoretical value for a call or a put option based on six variables.

- the strike price of an option

- the current stock price

- the time to expiration

- the risk-free rate

- the volatility

- the type of option

This mathematical equation estimates the theoretical value of derivatives based on other investment instruments, considering the impact of time and other risk factors.

- Though usually accurate, the Black-Scholes model makes certain assumptions that can lead to prices that deviate from the real-world results.

- The standard BSM model is only used to price European options, as it does not consider that traders could exercise American options before the expiration date.

C=S N\left(d_{1}\right)-K e^{-r t} N\left(d_{2}\right)

where:

d_{1}=\frac{\ln \frac{S_{t}}{K}+\left(r+\frac{\sigma_{v}^{2}}{2}\right) t}{\sigma_{s} \sqrt{t}}

and

d_{2}=d_{1}-\sigma_{s} \sqrt{t}

and

$C=$ Call option price

$S=$ Current stock (or other underlying) price

$K=$ Strike price

$r=$ Risk-free interest rate

$t=$ Time to maturity

In/Out-of-the-Money

Definitions

In options trading, the difference between "in the money" (ITM) and "out of the money" (OTM) is a matter of the strike price’s position relative to the market value of the underlying stock, called its moneyness.

An ITM option is one with a strike price that has already surpassed the current stock price. An OTM option has a strike price that the underlying security has yet to reach, meaning the option has no intrinsic value.

Strategies

Compared to OTM options, ITM options

- have higher intrinsic value

- priced higher than OTM options in the same chain

- can be immediately exercised.

OTM are nearly always less costly than ITM options, making them more desirable to traders with smaller amounts of capital.

OTM options are more commonly traded for strategies such as covered calls or protective puts.

How Do Factors Affect Option Prices

Volatility

An increase in volatility leads to higher option values. This is because the extremes of positive outcomes, from which the holder may benefit, become more probable. Although extreme moves in the "wrong" direction (from the option holder’s viewpoint) also become more likely, the option holder always has the right – but not the obligation – to exercise (or not exercise) the option.

if volatility ↑ then put option price ↑

if volatility ↑ then call option price ↑

This is because uncertainty pushes the odds of an outcome higher.

Risk-Free Rate

if risk-free rate ↑ then put option ↓

if risk-free rate ↑ then call option ↑

Underlying

As the value of the underlying security rises, a call will generally increase. However, the value of a put will generally decrease in price. A decrease in the underlying security’s value generally has the opposite effect.

if market price of the underlying ↑ then put option ↓

if market price of the underlying ↑ then call option ↑

positive outcomes → option holders benefit from it

negative outcomes → option don’t have to exercise the option

Strike Price

Strike price determines whether an option has intrinsic value. An option’s premium (intrinsic value plus time value) generally increases as the option becomes further in-the-money. It decreases as the option becomes more deeply out-of-the-money.

Time until expiration

Time until expiration, affects the time value component of an option’s premium. Generally, as expiration approaches, the levels of an option’s time value decrease or erode for both puts and calls. This effect is most noticeable with at-the-money options.

Volatility

Definition

Volatility refers to the fluctuations in the market price of the underlying asset. For continuous outcomes represented by probability, volatility can show how wide or narrow the distribution is.

An option will have a continuous range of possible outcomes beyond the point where it goes into the money. As we are seeking probability information, we need to specify our expectation of how wide or narrow the distribution will be. The width of the probability distribution reflects option volatility (or "vol") and is a key factor in option valuation.

Volatility is measured by the annualised standard deviation of daily returns for the underlying instrument. Notice that we use daily returns, not prices, to measure volatility. This is done for the following reasons:

- Returns, expressed in percentage terms, provide information that is comparable across instruments

- Returns can be positive or negative, whereas prices can only be positive

Implied Volatility

Implied volatility is used in options pricing to show the expected volatility of the option’s underlying stock over the option’s life.

It is a metric that captures the market’s view of the likelihood of changes in a given security’s price.

Investors can use implied volatility to project future moves and supply and demand and often employ it to price options contracts.

Pros and Cons of Implied Volatility

Pros

- Quantifies market sentiment, uncertainty

- Helps set options prices

- Determines trading strategy

Cons

- Based solely on prices, not fundamentals

- Sensitive to unexpected factors, news events

- Predicts movement, but not direction

Volatility and the Market

Implied volatility usually increases in bearish markets and decreases when the market is bullish.

Implied Volatility vs Historical Volatility

Implied volatility isn’t the same as historical volatility (realised volatility or statistical volatility), which measures past market changes and their actual results.

See implied-vs-historical-volatility

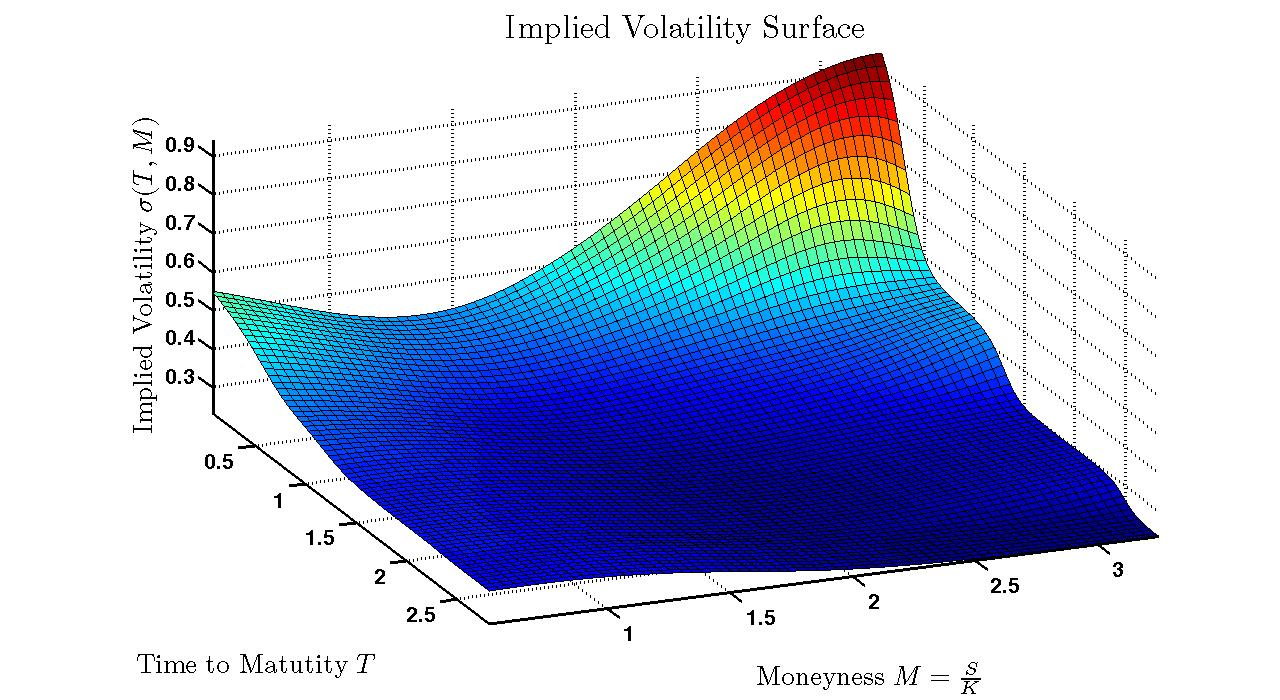

Volatility Surface

The volatility surface refers to a three-dimensional plot of the implied volatilities of the various options listed on the same stock.

X Time to maturity Y Moneyness Z Volatility

image source: https://www.mathworks.com/matlabcentral/fileexchange/23316-volatility-surface

where

Moneyness is a term to describe whether a contract is either "in the money", "out of the money", or "at the money".

- A call option is said to be "in the money" when the future contract price exceeds the strike price.

- A call option is "out of the money" when the future contract price is below the strike price.

The volatility surface varies over time and is far from flat, demonstrating that the assumptions of the Black-Scholes model are not always correct.

The Greeks

Delta

Delta can be thought of as a probability. For instance, a 30-delta option has roughly a 30% chance of expiring in the money. Delta also measures the option’s sensitivity to immediate price changes in the underlying. The price of a 30-delta option will change by 30 cents if the underlying security changes its price by $1.

Gamma

Gamma is the speed the option for moving in or out of the money. Gamma can also be thought of as the movement of the delta.

Vega

Vega is a Greek value that indicates the amount by which the option price would be expected to change based on a one-point change in implied volatility.

Theta

Theta is the Greek value that indicates how much value an option will lose with the passage of one day.

Option Strategy Examples

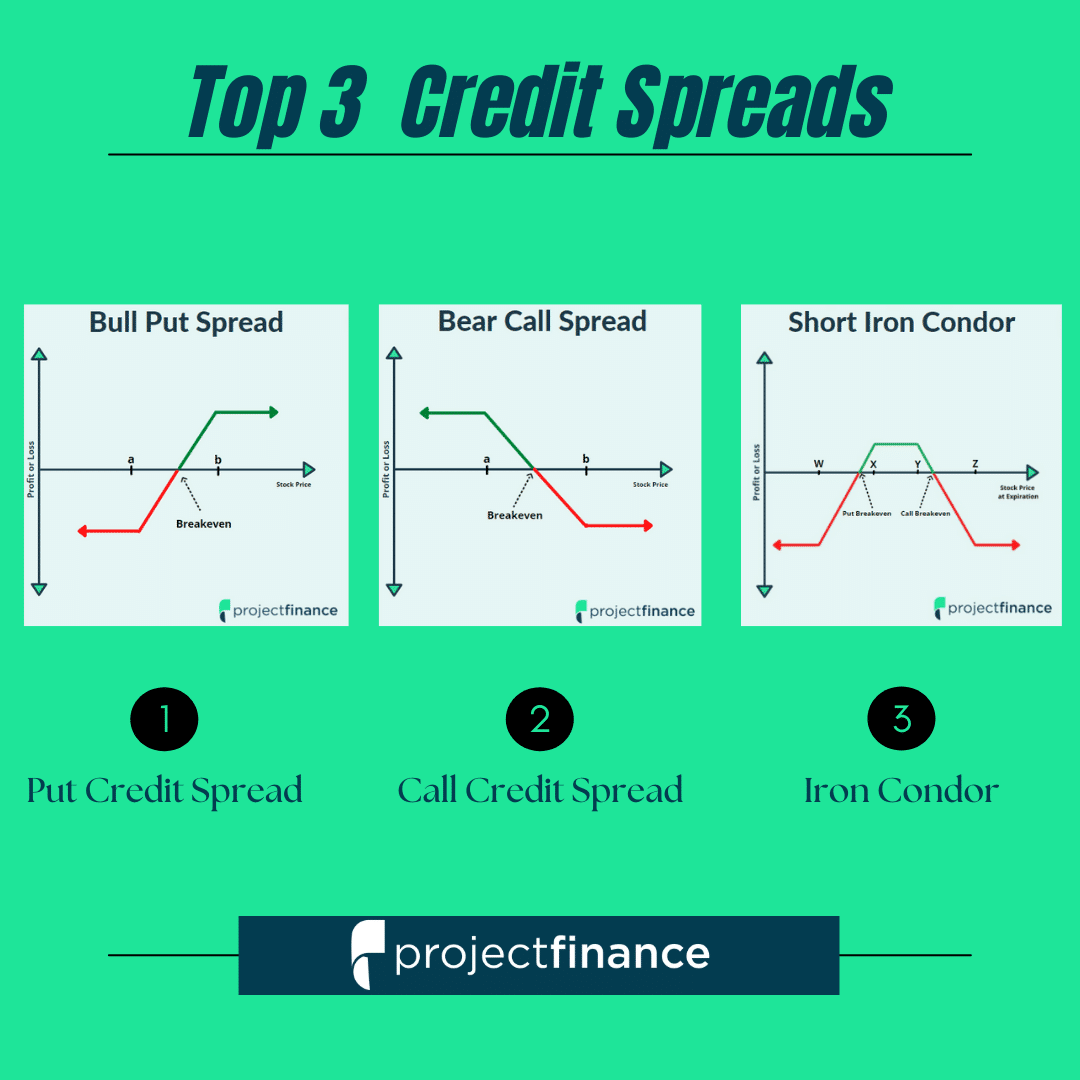

Spreads

Bull Call Spread

-

Buying a call

-

Simultaneously selling another call with a higher strike price and the same expiration.

The spread is profitable if the underlying asset increases in price, but the upside is limited due to the short call strike.

The benefit, however, is that selling the higher strike call reduces the cost of buying the lower one.

Bear Put Spread

You are buying a put and selling a second put with a lower strike and the same expiration.

Calendar Spread / Time Spread.

It is known as a Calendar Spread / Time Spread if you buy and sell options with different expirations.

image source: https://www.projectfinance.com/wp-content/uploads/2022/01/Top-3-Option-Credit-Spreads.png

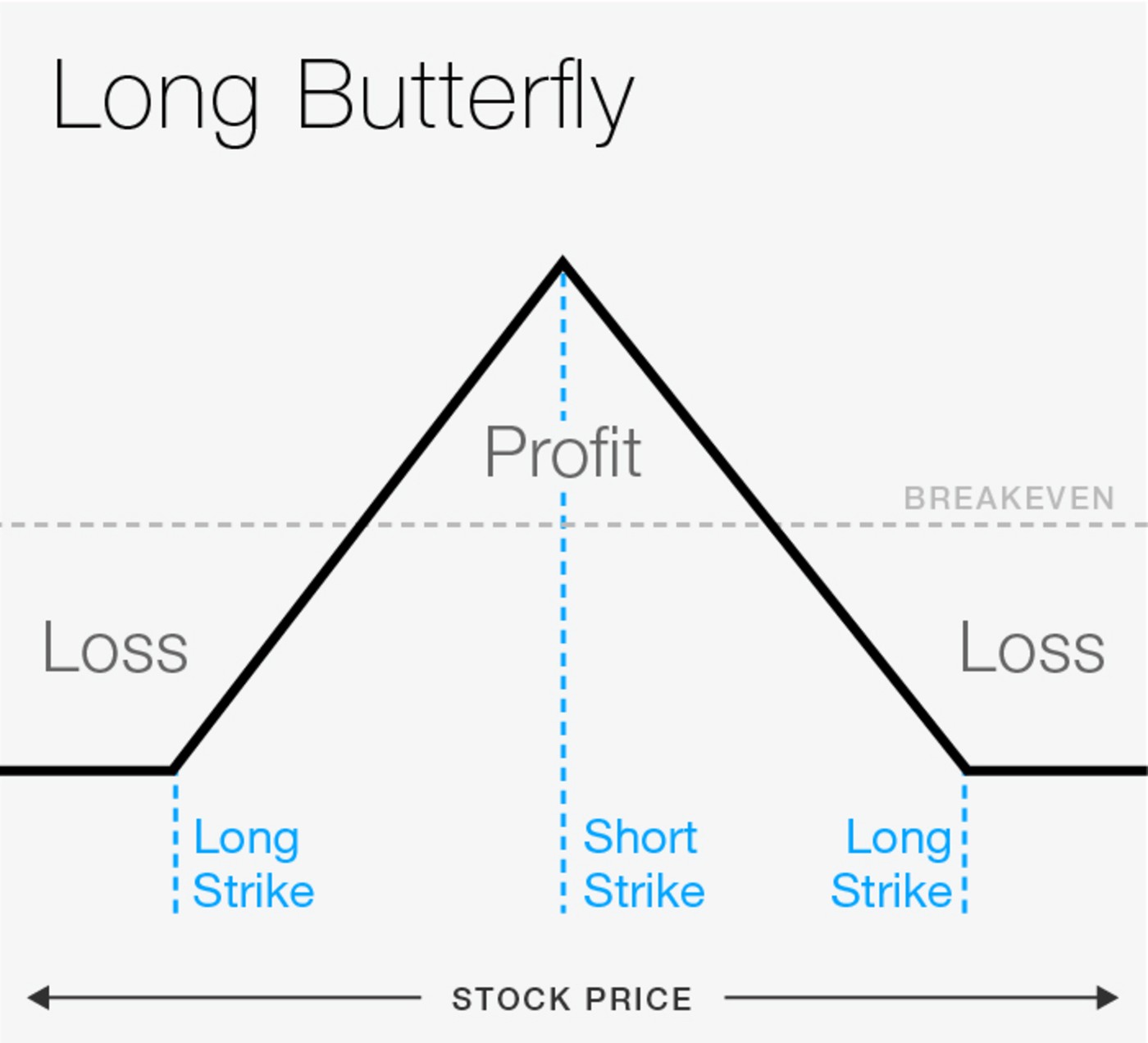

Butterflies

🦋 A butterfly consists of options at three strikes, equally spaced apart, wherein all options are of the same type (either all calls or all puts) and have the same expiration. In a long butterfly, the middle strike option is sold, and the outside strikes are bought in a ratio of 1:2:1 (buy one, sell two, buy one).

If this ratio does not hold, it is not a butterfly. The outside strikes are commonly referred to as the butterfly’s wings, and the inside strike as the body. The value of a butterfly can never fall below zero. The condor is closely related to the butterfly—the difference is that the middle options are not at the same strike price.

image source: https://tickertapecdn.tdameritrade.com/assets/images/pages/lg/long-butterfly-option-tt210730_f1.jpg

References

What are Options in Finance?. (2016). Retrieved 27 June 2022, from https://www.wallstreetmojo.com/what-are-options/

How Does Implied Volatility Impact Options Pricing?. (2022). Retrieved 27 June 2022, from https://www.investopedia.com/ask/answers/062415/how-does-implied-volatility-impact-pricing-options.asp#:~:text=Volatility%20refers%20to%20the%20fluctuations,prices%20behave%20in%20certain%20ways.

How Implied Volatility (IV) Helps You to Buy Low and Sell High. (2022). Retrieved 27 June 2022, from https://www.investopedia.com/terms/i/iv.asp

The Value of an Option – Derivatives | CFA Level 1 Exam – AnalystPrep. (2020). Retrieved 27 June 2022, from https://analystprep.com/cfa-level-1-exam/derivatives/the-value-of-an-option/#:~:text=As%20time%20the%20risk%2Dfree,of%20a%20put%20option%20decreases.

What is an Option Chain & Understanding How to Read Them. (2022). Retrieved 27 June 2022, from https://www.merrilledge.com/investment-products/options/what-is-an-option-chain

Understanding Option Pricing: Intrinsic & Time Value. (2022). Retrieved 27 June 2022, from https://www.merrilledge.com/investment-products/options/options-pricing-valuation#:~:text=An%20option’s%20premium%20is%20comprised,dividends%20and%20interest%20rate%20risks.

Option Trading Basics. (2022). Retrieved 27 June 2022, from http://www.trade-stock-option.com/option-trading-basics.html

A Beginner’s Guide to Call Buying. (2022). Retrieved 27 June 2022, from https://www.investopedia.com/trading/beginners-guide-to-call-buying/

Option Dojo – How to trade options. (2022). Retrieved 27 June 2022, from https://www.option-dojo.com/en/

McPhee, P. (2022). Options and Delta Hedging. Retrieved 27 June 2022, from https://www.optiontradingtips.com/options101/delta-hedging.html

Options & Derivatives Trading. (2022). Retrieved 27 June 2022, from https://www.investopedia.com/options-and-derivatives-trading-4689663

Derivatives – Options & Futures (2022). Retrieved 27 June 2022, from https://www.coursera.org/learn/derivatives-options-futures

An Essential Options Trading Guide. (2022). Retrieved 27 June 2022, from https://www.investopedia.com/options-basics-tutorial-4583012

How Does Implied Volatility Impact Options Pricing?. (2022). Retrieved 27 June 2022, from https://www.investopedia.com/ask/answers/062415/how-does-implied-volatility-impact-pricing-options.asp#:~:text=Volatility%20refers%20to%20the%20fluctuations,prices%20behave%20in%20certain%20ways.

Implied vs. Realised Volatility. (2022). Retrieved 27 June 2022, from https://www.tastytrade.com/news-insights/implied-vs-realized-volatility#:~:text=Implied%20volatility%20represents%20the%20current,over%20a%20defined%20past%20period.

Learn About Implied Volatility. (2022). Retrieved 27 June 2022, from https://www.investopedia.com/articles/optioninvestor/08/implied-volatility.asp

Options Exercise . (2022). Retrieved 27 June 2022, from https://www.optionseducation.org/referencelibrary/faq/options-exercise

The Value of an Option – Derivatives | CFA Level 1 Exam – AnalystPrep. (2020). Retrieved 27 June 2022, from https://analystprep.com/cfa-level-1-exam/derivatives/the-value-of-an-option/#:~:text=As%20time%20the%20risk-free,of%20a%20put%20option%20decreases.