CDS 2/3 Pricing

Main Page

Credit Default Swap, Index and Index Option

Background

CDS contracts in general trade based on a spread, representing the cost a protection buyer has to pay the protection seller (the premium* paid for protection).

:green_book: Glossary

CDS Spread / Premium – The amount paid by the Protection Buyer to the Protection Seller, typically denominated in basis points and paid quarterly.

Probabilities

Imagine the case of a one-year CDS with an effective date t_{0} with four quarterly premium payments occurring at times t_{i}

t_i = The i^{th} payment date

p_i = Survival probability from t_{0} to t_{i}

graph

t0((t0)) --"Default (possibility: 1 - p1)" --> t1_1((t1))

style t0 fill:#82D9C9,stroke:#82D9C9

style t1_1 fill:#F28DA8,stroke:#F28DA8

t0((t0)) --"Payment (possibility: p1)" --> t1_2((t1))

style t1_2 fill:#82D9C9,stroke:#82D9C9

t1_2((t1)) --"Default (possibility: 1 - p2)" --> t2_1((t2))

style t2_1 fill:#F28DA8,stroke:#F28DA8

t1_2((t1)) --"Payment (possibility: p2)" --> t2_2((t2))

style t2_2 fill:#82D9C9,stroke:#82D9C9

t2_2((t2)) --"Default (possibility: 1 - p3)" --> t3_1((t3))

style t3_1 fill:#F28DA8,stroke:#F28DA8

t2_2((t2)) --"Payment (possibility: p3)" --> t3_2((t3))

style t3_2 fill:#82D9C9,stroke:#82D9C9

t3_2((t3)) --"Default (possibility: 1 - p4)" --> t4_1((t4))

style t4_1 fill:#F28DA8,stroke:#F28DA8

t3_2((t3)) --"Payment (possibility: p4)" --> t4_2((t4))

style t4_2 fill:#82D9C9,stroke:#82D9C9

t4_2 --> contractEnd(Contract End)

style contractEnd fill:#82D9C9,stroke:#82D9C9

Present value

PV Calculation

According to the fair value approach, the present value of both sets of cash flows should be identical.

PV_{{fixed }}=PV_{{float}}

- The fixed stream from the buyer is only paid until the earlier of a credit event or the maturity of the contract

- The ‘floating’ payment from the seller only occurs in case of a credit event

{PV}_{{fixed}}=sum_{{i}=1}^{{n}} {Spread} * {DF}_{{i}} * {p}_{{i}} * alpha{{i}}

{PV}_{{float }}=sum_{{i}=1}^{{n}}(1-{R}) * {DF}_{{i}} *({p}_{{i}-1}-{p}_{{i}})

where

t_i = The i^{th} payment date

p_i = Survival probability from t_{0} to t_{i}

n = Number of coupon periods

Spread = CDS spread – The annual amount the buyer pay expressed as a percentage of the notional amount

DF_i = Risk free discount factor

p_i = Survival probability from t_{0} to t_{i}

\alpha_{{i}} = Accrual factor from time t_{i-1} to t_{i}

R = Recovery rate – percentage of notional repaid in event of default

(p_{i-1} - p_{i}) = Marginal default probability from t_{i-1} to t_{i}

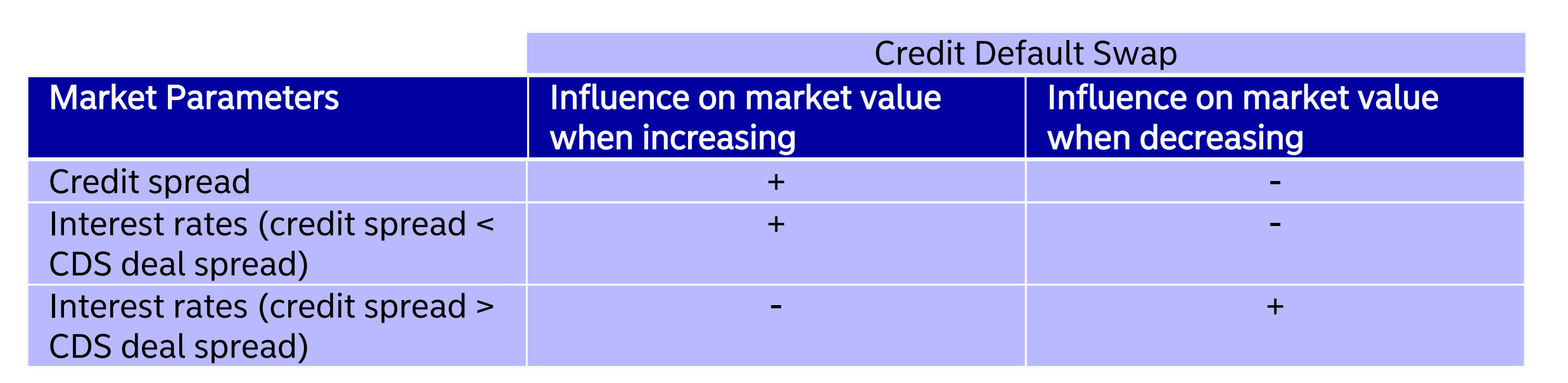

CDS Spread

CDS Spread is the buyer’s annual amount expressed as a percentage of the notional amount.

The value of the CDS contract increases for the protection buyer if the spread increases.

{PV}_{{fixed}}\textcolor{red}{\uparrow} =sum_{{i}=1}^{{n}} {Spread} \textcolor{red}{\uparrow} * {DF}_{{i}} * {p}_{{i}} * \alpha{{i}}

Hazard Rate

Hazard Rate is the conditional probability of default in Period n for a particular entity, given that this entity has survived until the beginning of Period n. Hazard rates are’ backed out’ of a CDS spread curve and ‘bootstrapped’ to create a term structure of Hazard rates.

This term structure of Hazard rates is then translated into a term structure of Survival Probabilities and a term structure of Non-conditional Default Probabilities. The former weighs the CDS’ premium (or ‘fee’) leg, while the latter weighs the protection (or ‘contingent’) payment leg.

The PV of each leg is discounted to find the MTM value of a CDS contract.

Survival probability

It is the probability of an entity not defaulting in period n and subsequent periods. These probabilities are modelled as a function of Hazard Rates. A term structure of survival probabilities is used to quantitatively weigh the premium (or fee) leg when valuing a CDS transaction.

The probabilities p_{i} can be calculated using the credit spread curve. The probability of no default occurring over some time from {t} to t+\Delta t decays exponentially with a time constant determined by the credit spread.

The riskier the reference entity, the greater the spread and the more rapidly the survival probability decays with time.

p=exp (-s(t) \Delta t /(1-R))

where

s(t): the credit spread zero curve at time t.

Recovery rate

Recovery Rate represents the value post-default. It estimates the percentage of par value that bondholders will receive after a credit event. i.e. the principal and accrued interest on defaulted debt can be recovered. It impacts expected cash flows.

The recovery rate is expressed as a percentage of face value. The recovery rate can also be defined as the security value when it emerges from default or bankruptcy.

CDS for investment-grade bonds generally assume a 40% recovery rate when valuing CDS trades. However, CDS for lower-rated bonds are more dynamic and often reflect lower estimated recovery rates.

Calculation

Recovery rates are affected by

- The seniority of the debt obligation – Nature of the industry of the borrower

- Legal environment

- Level of defaults (the more defaults, the lower the recovery rates)

R in investment securities

For investment-grade names, recovery is generally assumed to be 40%. As the probability of default is low, the recovery rate is at best estimation.

R in distressed securities

The probability of default of distressed securities is higher. The recovery tends to be more precisely defined.

Distressed securities

Distressed securities are trading with an upfront payment and a standard running spread.

:blue_book: For example, instead of trading a name with a spread of 1000, the protection buyer will generally pay a running coupon of 500 and an upfront amount to compensate the seller for the difference between 1000 and 500 for the life of the trade.

In a five year trade maturing on 20 September 2014 entered on 13 July 2009, the upfront amount will be approximately 16.75 points or $167,500 for $1 million of protection.

Market Parameters

Mark-to-Market value

The contingency of the payments also needs to be considered when calculating the fair/mark-to-market (MTM) value of a position.

{MTM}=sum_{{i}=1}^{{n}} \text { Net Spread } * {DF}_{{i}} * {p}_{{i}} * \alpha_{{i}}

Net spread

Net interest spread refers to the difference in borrowing and lending rates of financial institutions (such as banks) in nominal terms.

:blue_book: For example

An investor sold 5Y protection at a spread level of 150 bps, and subsequently, CDS spreads tightened to $100 bps

- The investor could now buy back the protection sold and lock in a spread of 50 bps per annum

- However, as ‘fixed’ payments are only made until the earlier of a credit event or the maturity of the contract, the net premium payments have to be weighed by the probability of there being no credit event before the cash flow dates (survival probability)

Implied Default Probabilities

Is this CDS cheap or expensive?

Given that

\text{Credit Spread} = \text{Probability of Default} * \text{(1 - Recovery Rate)}

Then

\text { Probability of Default }=\frac{\text { Credit Spread }}{(1-\text { Recovery Rate })}

So: If we have

- market prices

- recovery rate (can be assumed)

Then we can

- derive implied default probabilities from the market

- compare them with either historical periods or with our predictions

- decide whether credits are cheap or expensive

CDS in Terms of a Bond Position

Theoretically, the CDS premium should equate to the spread over Libor for the issuer’s floating rate note trading at par.

A fixed-rate corporate bond has interest rate, credit and financing risk. If we swap the returns to floating and finance the bond, the CDS premium equals the spread paid on the asset swap.

CDS Basis is the difference between CDS spreads / Premium and bond asset swap spreads (ASW) [1]. The basis illustrates positive and negative basis arbitrage trades.

graph LR

Bond(Bond)

AssetSwap(Asset Swap)

Buyer(Protection and Bond Buyer)

ProtectionSeller(Protection Seller)

Financing(Financing)

Bond --" Coupon "--> AssetSwap

AssetSwap --" Par "--> Bond

AssetSwap --"Libor + Spread" --> Buyer

Buyer --"Par" -->AssetSwap

ProtectionSeller --"Protection" --> Buyer

Buyer --"Premium"-->ProtectionSeller

Financing --"Par"--> Buyer

Buyer --"Repo [2]" --> Financing

:green_book: Glossary

[1] Bond Asset Swap Spread – An asset swap involves a fixed rate swap in return for a floating rate. The fixed-rate is derived from an asset. The floating rate is composed of a spread over LIBOR (or another floating benchmark). The asset swap spread (gross spread) is derived by valuing a bond’s cash flows via the swap curve’s implied zero rates. This gross spread is the basis point amount added to the swap curve, which causes a bond’s computed value to equal the bond’s market price. It is comparable to a CDS spread in that it is interest-rate insensitive.

[2] Repo – a short-term secured loan

Negative Basis (CDS < ASW spread)

It occurs when the ASW or Z-Spread of a bond is wider / larger than the CDS spread.

- Assumption of Libor flat funding [1] is not true in stressed markets [2]

- Credit risk on CDS seller – correlation[3] with reference entity

- CLN[4] / synthetic CDO [5] [6] issuance

:green_book: Glossary

[1] Flat funding – Fixed funding

[2] Stressed markets – means a period of significant short-term change in the price or volume of Orders

[3] Correlation – Statistical relationship, whether causal or not, between data

[4] CLN – Credit-linked note – A security with an embedded credit default swap permitting the issuer to shift specific credit risk to credit investors

[5] CDO – A collateralized debt obligation (CDO) is a complex structured finance product backed by a pool of loans and other assets and sold to institutional investors.

[6] Synthetic CDO – A synthetic CDO is a variation of a CDO that generally uses credit default swaps and other derivatives to obtain its investment goals.

Positive Basis (CDS > ASW spread)

- CDS spreads for IG names cannot be negative

- Efficient shorting via CDS

- CDS prices move faster on bad news

- Convertible bond hedging