CDS 1/3 Introduction

Main Page

Credit Default Swap, Index and Index Option

CDS

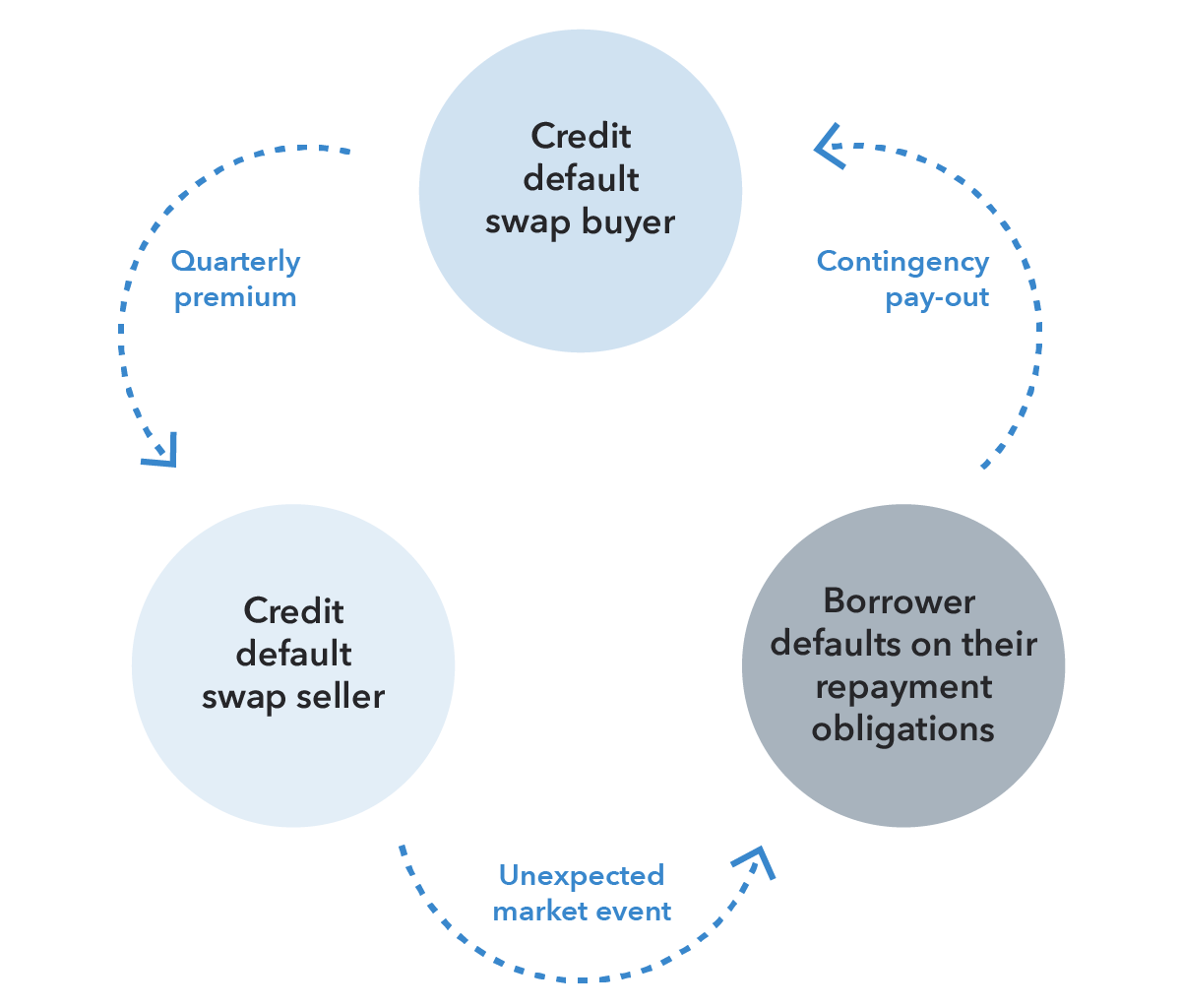

A credit default swap [1] (CDS) is the most common form of credit derivative [2]. Most of them are over-the-counter (OTC) contracts.

It allows one party to transfer an asset’s credit risk to another party without transferring ownership of the underlying asset. i.e. Allow agents to increase or decrease credit exposure without participating in any underlying loan.

image source: https://a.c-dn.net/c/content/dam/publicsites/igcom/uk/images/ContentImage/credit_default_swap.png

Over-the-counter (OTC)

OTC refers to how securities are traded via a broker-dealer network instead of a centralised exchange.

-

Most of the CDSs are traded on an OTC basis

-

Some of them are on other platforms like SEF and MTF – where the platforms do not join as principal roles

Terms of Trade

There are different kinds of credit derivatives, but their terms usually would have

- The Reference Entity

- The underlying entity on which protection is bought/sold

- The Reference Obligation

-

This may not be the actual deliverable instrument at default

-

Its maturity may not equate with that of the CDS contract at trade inception.

-

It represents the lowest seniority of bonds that can be delivered in case of default

- A Notional Amount

- the amount of credit risk bought/sold

-

The Tenor of the trade (with 5-year tenors generally being the most liquid)

-

The definitions of "credit event."

-

Cash / physically settled (including what physical bond can be delivered)

- ….

Long? Short?

You are either ‘long’ or ‘short’ of a financial instrument when you place a trade.

Long: makes a profit if an asset’s market price increases. They are usually used in context as ‘taking a long position’ or ‘going long’.

Short: describes a trade that will incur a profit if the traded asset falls in price. It is also often referred to as going short, shorting or sometimes selling.

Short / Bear CDS = Protection / CDS Seller = Long Reference

Long / Bull CDS = Protection / CDS Buyer = Short Reference

image source: https://www.investorsunderground.com/wp-content/uploads/2016/05/longshort.jpg

:green_book: Glossary

Position – the amount of a security, commodity, currency etc., that is owned or sold short by an individual, dealer, institution, or other entity.

Market Player Overview

The market players can be divided into the following.

-

End-Users: buyer / seller

-

Trading Intermediaries

-

Regulatory (like ISDA) and governance bodies (like CFTC) – legal framework / market convention / clearing infrastructure

Reference Entity

- Reference Entity refers to the legal entity that is the subject of a CDS contract,

i.e.

-

the company for which credit protection is bought

-

the underlying borrower

-

Its underlying credit risk is being transferred.

-

The reference entity can be the issuer or the guarantor of the debt.

Protection Period

Extended:

-

From – a few months before the trade date

-

To – maturity date

Buyer

Example: – Banks are the biggest buyers.

Long / Short

Buyers will benefit when credit quality deteriorates and spreads rise.

Motivation

(see details in #Usage of a CDS)

-

Regulatory capital relief

-

Credit risk management / hedging (protection against credit events )

-

Allow credit trading

-

Can focus on interest rate only

-

Keep the bond in the portfolio while reducing the risk

Details

So buyers

-

Can swap or offset their credit risk with the seller.

-

Short the credit risk.

-

Can also speculate that the cost of protection will rise and profit from selling the CDS contract at a higher price than was paid.

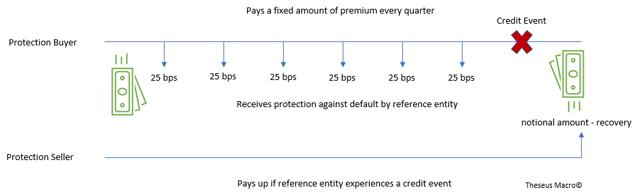

At the start

Payment of the premium

Before a credit event

-

Needs to make fixed periodic payments/premiums as a standardised coupon (Fee Leg).

-

Standardised coupons facilitate the fungibility of different contracts.

-

Fixed coupons

-

100 and 500bp in the US

-

25,100,500, or 1,000 bp in Europe

- Gets interests and principles from the reference entity.

graph LR

ReferenceEntity(Reference Entity) --"Interet and prinicpal" --> Buyer(Buyer)

Buyer(Buyer) --"Fixed cash payments"--> Seller(Seller);

After a credit event

-

Delivers a bond of seniority at least equal to that of the reference obligation.

-

If there are multiple bonds deliverable, the protection buyer will most likely deliver the cheapest bond to the protection seller.

-

Receive – 100% of the par value of the underlying reference obligation.

-

Pay – recovery value (Reference obligation at x% of par + accrued CDS interest), i.e. Default Leg (DL).

graph LR

ReferenceEntity(Reference Entity) --"Default" --> Buyer(Buyer)

Buyer(Buyer) -- "Reference obligation at x% of par +

accrued CDS interest"--> Seller(Seller);

Seller(Seller) -- "100% of the par value of the underlying reference obligation"--> Buyer(Buyer) ;

Seller

Example: Hedge funds are the major sellers

Motivation

(see details in #Usage of a CDS)

-

Generate income by taking on credit risk exposure

-

Can hedge without holding the asset

-

Diversity portfolio

Long / Short

Selling a CDS means selling protection (and receiving premiums) and is equivalent to owning or being long the bond (“long risk”).

If reference credit quality improves, this position will generate positive mark-to-market present value changes.

And credit spreads narrow during the life of the trade.

Details

Protection sellers are in a similar position to a lender but without the inconvenience of funding the position or interest rate risk.

i.e. increase their own credit risk

So the sellers

-

Long the credit risk.

-

Exposed to the credit risk of the reference entity.

-

If such an event occurs, it triggers the Protection Seller’s settlement obligation, either cash or physical.

-

Insurance companies are the biggest sellers because they want to

-

Increase diversification

-

Enhance yield (a cheaper alternative to bonds)

-

Match maturity profile of liabilities

source: https://static.seekingalpha.com/uploads/2020/7/38699106_15955172912819_rId11.png

Trading Intermediaries

Responisbility

Facilitate execution

Dealer / Broker

Dealers are people or firms who buy and sell securities for their account, whether through a broker or otherwise. A dealer acts as a principal in trading for its account instead of a broker who acts as an agent who executes orders on behalf of its clients.

The dealer is generally the calculation agent in contracts between CDS dealers and end-users by market convention. The protection seller is generally the calculation agent in contracts between CDS dealers.

Market

Interdealer transactions represent the majority of CDS volume.

Other Terms

Single Name / Multi-Name

A single-name CDS is a derivative in which the underlying instrument is a reference obligation or a bond of a particular issuer or reference entity. i.e. based on a single reference name

In the market of 2014

- single name:55%

- multi name:45%

Markit

This note is based on the tutorial of Markit

Markit is an independent entity that is certainly influential in determining the trading landscape and takes responsibility for important elements such as reference data and indices.

Liquididy

Liquidity means a person or company has sufficient liquid assets to pay the bills on time.

Disotrion

Departure from the ideal of perfect competition that therefore interferes with economic agents maximising social welfare when they maximise their own

Fungibility

Fungibility is the ability of a good or asset to be interchanged with other individual goods or assets of the same type. Fungible assets simplify the exchange and trade processes, as fungibility implies equal value between the assets.

-

Fungibility is the ability of a good or asset to be readily interchanged for another like-kind.

-

Like goods and assets that are not interchangeable, such as owned cars and houses, are non-fungible.

-

Money is a prime example of something fungible, where a $1 bill is easily convertible into four quarters or ten dimes, etc.

Netting

Netting entails offsetting the value of multiple positions or payments due to be exchanged between two or more parties.

It can

-

help participants reduce their counterparty exposure by offsetting contracts with negative market values against contracts with positive market values.

-

reduce the gross market values of credit derivates can be seen in the diagram opposite

Netting is used in CDS.

Counterparty

A counterparty is the other party that participates in a financial transaction, and every transaction must have a counterparty for the transaction to go through.

Central Counterparty Clearing House (CCP)

CCP is an entity that helps facilitate trading in various European derivatives and equities markets.

for Credit derivatives, transactions are executed between market participants and then subsequently be cleared through a CCP, which will act as an intermediary principal

Derivative

Definition

A broad term describing financial instruments that "derive" their value from an underlying asset or benchmark. Like Futures, Options, Swaps, Forwards, etc.

Credit Derivative

Since the 1990s, a credit derivative has been a financial contract that allows parties to minimise their exposure to credit risk. Credit derivatives consist of a privately held, negotiable bilateral contract traded over-the-counter (OTC) between two parties in a creditor/debtor relationship.

It can be used to reduce credit risk.

Credit derivatives allow participants to pay or receive a credit spread without touching the underlying position.

Otc derivatives by notional amounts

image source: https://www.researchgate.net/

Collateral

Collateral is an asset that a lender accepts as security for extending a loan. If the borrower defaults, then the lender may seize the collateral.

A CDS can be unsecured (without collateral) and be at higher risk for default.

Swap

Swap: An agreement between two parties to exchange future cash flows or credit risk.

Swap Quote

Swaps are typically quoted in a swap spread, which calculates the difference between counterparty rates.

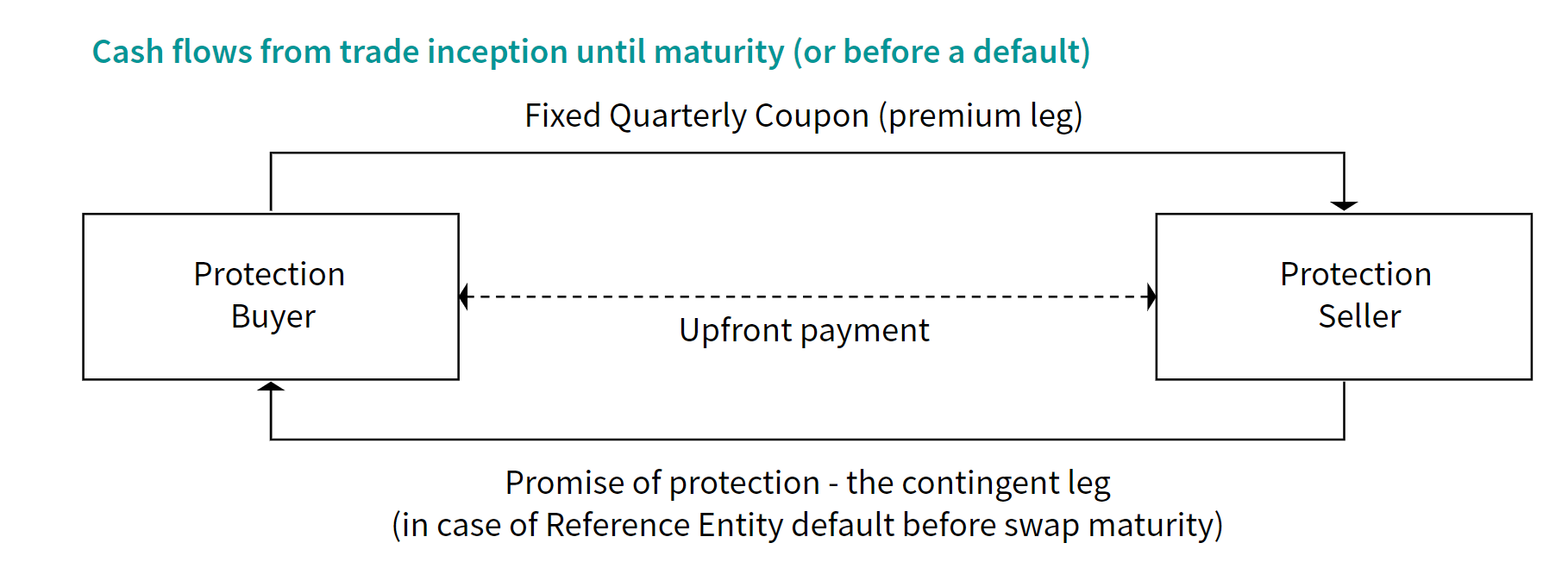

The swap legs

The two legs of a CDS are known as the

-

“premium leg” (relating to the periodic payments made by the Protection Buyer)

-

“contingent leg” (relating to the amount the Protection Seller pays out if a credit event is triggered).

Swap Yield

Sometimes we assess the credit spread in terms of the yield spread over the swap market. There is no constraint on supply, so wap rates are not subject to the same liquidity distortion as an individual bond issue.

So usually (not always), swap yields are slightly higher than government bond yields under the same condition, given that swaps are based on interbank risk.

Swap Rate

Definition

A swap rate is the rate of the fixed leg of a swap as determined by its particular market and the parties involved.

A swap rate denotes the fixed rate that a party to a swap contract requests for the obligation to pay a short-term rate, such as the Labor or Federal Funds rate.

When the swap is entered, the fixed rate will equal the value of floating-rate payments, calculated from the agreed counter-value.

Risk-Free vs Swap Rate

Usually, swap rates are higher than domestic government bond (risk-free) yields of the same maturity – they have a yield premium.

Asset Swap

Transactions in which the investor acquires a bond position and then enters into an interest rate swap with the bank that sold them the bond. The investor pays fixed and receives floating. This transforms the fixed coupon of the bond into a LIBOR-based floating coupon.

Asset Swap affect interest rate risk rather than credit risk

Credit Risk

Definitions

Credit Risk is the risk that the borrower of money fails to make timely payments of both interest and principal or meet contractual obligations.

Yield

Some of the credit risks are present in bond portfolios. The return (yield) on a fixed rate bond can be split into

-

Interest rate return – compensate the time value of money

-

Credit risk-return – compensates for the possibility of default

For government securities, the credit risk is usually very low.

governments can simply choose to print more money rather than the default

For more risky borrowers, the yield on their bonds will generally be greater than a government bond under the same conditions (maturity etc.).

Calculation

-

Credit risk was a static risk on the balance sheet.

-

The actual loss suffered by the lender is a function of both the probability of default (

p_i) and the recovery rate (R)

Credit Events

Credit events trigger settlement under the CDS contract.

-

Reference entity bankruptcy / insolvency

-

Governmental intervention

-

Failure to pay – The reference entity fails to make interest or principal payments when due, after the grace period expires

-

Obligation default – lender requires the full return of principal because of some default by the borrower

-

Obligation acceleration – debt must be paid ahead of schedule because the borrower did not adhere to the terms of the loan

-

Repudiation / Moratorium Usually in soveregin contracts

-

Restructuring – reorganises to consolidate its debt.

-

Liquidation

Credit default swaps do not protect against

-

interest rate changes

-

credit rating downgrading (it would increase the value of the contract)

-

Succession events (like merging)

Tenor / Maturity

Tenor refers to the length of time remaining before a financial contract expires. It is sometimes used interchangeably with the term maturity.

:arrow_up: Higher-tenor contracts are :arrow_up: riskier, and vice versa.

Most credit derivatives have original tenors of between one and five years.

Tenor vs. Maturity

Tenor:

-

The length of time remaining in a contract

-

Declines over time

Maturity:

-

The initial length of the agreement upon its inception

-

Constant

For example, if a 10-year government bond was issued five years ago.

-

Maturity would be ten years

-

Tenor—the time remaining until the end of the contract—would be five years. In this

Cash Flow

Upfront Payment

Upfront payment

-

is the initial lump sum payment made when entering a CDS transaction.

-

reflects the riskiness of the contract. So it tends to apply to transactions where the credit quality of the entity referenced is poor / where the perceived risk of the entity defaulting is high.

-

i.e. :arrow_down: perceived credit-worthiness :arrow_up: insurance premium and associated par CDS spread.

:blue_book: Example: if the annual coupon of the CDS is 50 basis points or 0.5%, and the fair spread / market price is around 60 bsp (0.6%), Then the protection buyer needs to pay (0.6%-0.5%) bsp to the protection seller

However, if the fair spread / market price is lower (like 40bsp / 0.4%), the protection seller pays an upfront equivalent to the present value of the excess 0.1%

Premium

The fixed premium (or what is called the spread) is composed of

-

the upfront amount

-

a standardised fixed coupon paid regularly over the life of the trade on specific dates – i.e. the periodic payment rate – Usually – paid quarterly; expressed as a basis points’ annual percentage of the notional principal

-

CDS premium is generally quoted as an annual spread

-

Like any other credit spread, it represents the market’s view on the creditworthiness of the reference entity.

-

CDS premium might be paid partly to the buyer as an upfront amount.

The term spread (premium) is slightly not good as it is not comparing against anything

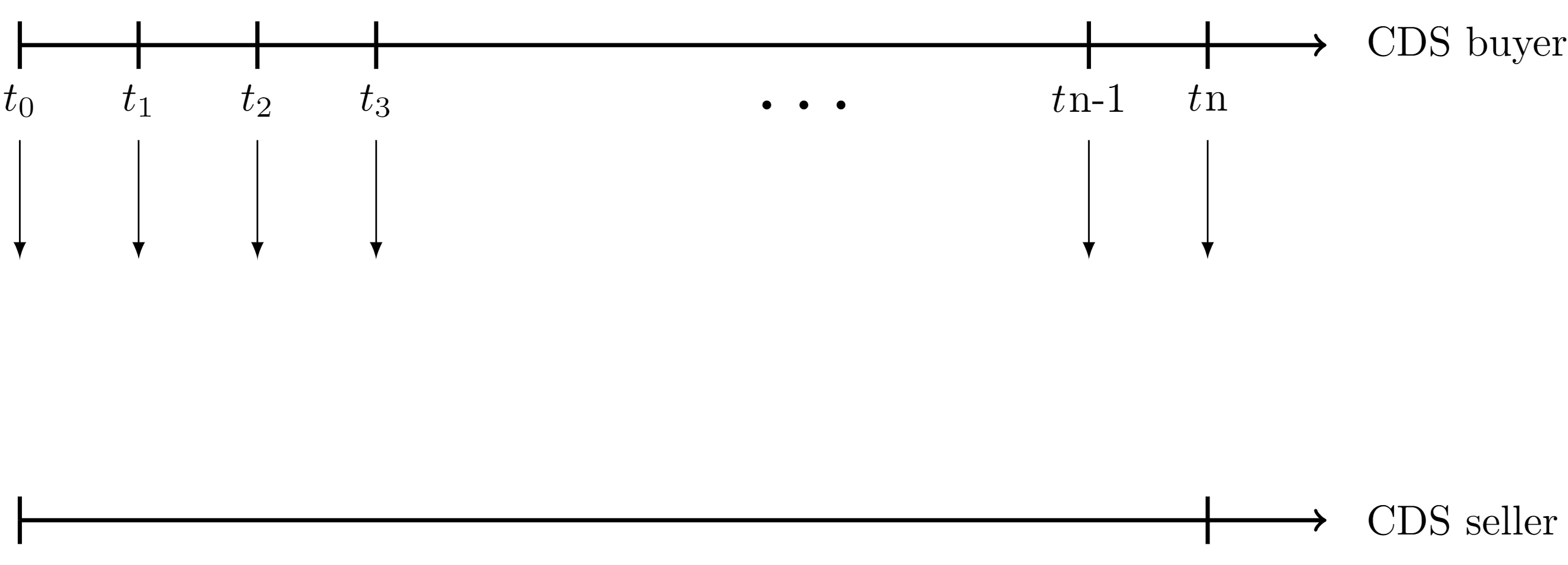

If default events never occurred

-

The price of that CDS is the sum of the discounted premium payments.

-

The contract survives until the maturity date.

If a default occurred

-

The default will happen during the effective date and maturity date.

-

The model considers the possibility of default at each payment date.

-

The model takes the present value of a series of cash flows weighted by their probability of non-default.

CDS Categories

| Reference entities | ||

|---|---|---|

| CDS | – | Senior unsecured bonds, usually issued by corporate or sovereign issuers |

| LCDS | Loan-only CDS | Limited strickly to syndicated loans. Senior secured in the capital structure |

| MCDS | Municipal CDS | Muni bond |

| ABCDS | Asset-Backed CDS | Asset-backed securities |

| PCDS | Preferred CD | Preferred securities |

Usage of a CDS

Risk-reducing

Credit risk

-

it is not eliminated

-

it is shifted to the CDS seller

-

it is reduced

:blue_book: For example, Moneylender A has made a loan to Borrower B with a mid-range credit rating. Lender A can increase the loan quality by buying a CDS from a seller with a better credit rating and financial backing than Borrower B. The risk has not gone away, but it has been reduced through the CDS.

graph

A( - A - <br> Money lender <br> CDS buyer) --"Lend money" --> B( - B - <br> Money borrower <br> Mid-range rating);

A( - A - <br> Money lender <br>CDS buyer) --"buy CDS" --> C( - C - <br> CDS seller <br> High-range rating);

Hedging

-

Allow capital or credit exposure to free up capacity and facilitate doing more business.

-

Manage the risk of default that arises from holding debt.

-

Banks should not overly concentrate on a particular borrower or industry and lay off some of this risk by buying a CDS.

Speculation

A CDS is

-

mostly traded on an OTC basis

-

non-standardised

-

not verified by an exchange

-

complex and often bespoke

Speculation: investors can trade the obligations of the CDS if they believe they can make a profit.

:blue_book: For example, A CDS earns $10k quarterly payments to insure a 10 million bond. The company that initially sold the CDS believes that the borrower’s credit quality has improved, so the CDS payments are high. The company could sell the rights to those payments and the obligations to another buyer and potentially profit.

Investing

-

Offer the opportunity to take a view purely on credit

-

Offer access to hard to find credit (limited supply of bonds, small syndicate)

-

Allows investors to invest in foreign credits without bearing unwanted currency risk

-

Require little cash outlay and therefore creates leverage

CDS Trading

-

CDS trades refer to a notional – the quantity of the underlying asset or benchmark to which the derivative contract applies.

-

It does not refer to any cash exchange at the time of the trade or the mark-to-market size of the trade.

-

It is akin to the amount of insurance bought, not the premium paid.

-

Single name contracts are trading using a fixed coupon, similar to indices and distressed names.

Commonly Confused Concepts

CDS Spread, Par Spread, Credit Spread Curve, Theoretical Spread, Bond Asset Swap Spread, Credit Spread

Spread – The difference between two prices, rates, or yields

Credit Spread

-

For more risky borrowers (like companies etc.) The yield on their bonds will generally be greater than gov bonds (compensate credit risk)

-

determined by credit level (will it default?) and recovery rate

-

For the debt instruments of the same seniority and maturity by the same entity, where risk seems the same, the credit spread can be different due to the debt. (like bond vs loan)

i.e. it is the additional "margin" over the risk-free rate

CDS Spread – The annual amount the buyer pay is expressed as a percentage of the notional amount.

Par Spread – The spread of a CDS contract that ensures the PV of the expected premium payments (fee leg) equals the PV of the expected default payment (contingent leg).

Credit Spread Curve – the credit spread curve for a unique reference entity/tier/currency/doc-clause combination over different nodes or tenors.

Theoretical Spread (Price) – aka ‘Intrinsic Value’ or ‘Fair Spread’ – the spread of an index implied by the underlying index constituents with currency, doc clause, day counts, coupon, coupon frequency, and maturity is identical to that of the index.

Bond Asset Swap Spread – An asset swap involves a fixed rate swap in return for a floating rate. The fixed-rate is derived from an asset. The floating rate is composed of a spread over LIBOR (or another floating benchmark). The asset swap spread (gross spread) is derived by valuing a bond’s cash flows via the swap curve’s implied zero rates. This gross spread is the basis point amount added to the swap curve, which causes a bond’s computed value to equal the bond’s market price. It is comparable to a CDS spread in that it is interest-rate insensitive.

Example:

if a gov bond is trading at a yield of 5% and the swap spread is 0.1%, then the swap rate is 5.1%

if a corporate bond is trading at a yield of 7%, it generates a spread to swaps of (7-5.1)%

:green_book: Glossary

LIBOR – London Interbank Offered Rate – An interest rate is fixed in the interbank market, representing how highly-rated banks lend to one another. (Has been replaced by other benchmarks.)

LCDS vs CDS

Compared to CDS, LCDS is

-

higher in the capital structure

-

usually with higher recovery rates (the main difference)

-

generally trade at tighter spreads

Insurance Contracts vs CDS

CDS is similar to insurance contracts on a corporation or sovereign entity debt

-

Insurance regulators regulate CDS

-

CDS is not necessary to own the underlying debt to buy protection using CDS

i.e. CDS are not tied to the ownership of a particular asset.

Buyers can buy protection for shorting assets. where –

asset ↓ (deterioration) -> value of protection contract ↑

asset ↑ (deterioration) -> value of protection contract ↓

Corporate bonds vs CDS

| Corporate Bonds | CDS | |

|---|---|---|

| Availability | Limited | Unlimited |

| Liquidity | Mixed, limited size | No maximum size |

| Maturities | Fixed dates | Standard dates |

| Investment | Cash / Repurchase agreement (repo[1]) | Swap (unfunded) / note[2] (funded) |

| Coupon | Fixed / Floating | Spread |

:green_book: Glossary

Repo – a short-term secured loan

Note – a legal document representing a loan made from an issuer to a creditor or an investor

Regulatory and Concerns

Concerns

Credit derivatives WERE notorious for complexity and opacity.

CDSs have played a key role as drivers of systemic risk. The excessive exposure of financial institutions to these derivative instruments during the subprime crisis led to a rapid transfer of credit risk worldwide, spreading to all areas of the global market for public and private debt.

During the financial crisis of 2008, the value of CDS was hit hard, and it dropped to $26.3 trillion by 2010 and $25.5 trillion in 2012

Regulatory

The reporting requirement for CDS trades applies to ALL CDS trades.

- CDS contracts are currently mostly traded over the counter (OTC) rather than on an exchange, raising concerns over counterparty risk.