CDS 3/3 Settlement

Main Page

Credit Default Swap, Index and Index Option

Definition

A settlement means what occurs in the case of a credit event.

If a credit event occurs, then CDS contracts can be physically settled or cash-settled, depending on the terms of the contract.

Traditionally, CDS specified physical delivery. Numerous auctions have been held to allow cash settlement in the last few years.

graph

t0((t0)) --"Default" --> t1_1((t1))

style t0 fill:#82D9C9,stroke:#82D9C9

style t1_1 fill:#F28DA8,stroke:#F28DA8

t0((t0)) --> t1_2((t1))

style t1_2 fill:#82D9C9,stroke:#82D9C9

t1_2((t1)) --"Default " --> t2_1((t2))

style t2_1 fill:#F28DA8,stroke:#F28DA8

t1_2((t1)) --> t2_2((t2))

style t2_2 fill:#82D9C9,stroke:#82D9C9

t2_2((t2)) --"Default " --> t3_1((t3))

style t3_1 fill:#F28DA8,stroke:#F28DA8

t2_2((t2)) --> t3_2((t3))

style t3_2 fill:#82D9C9,stroke:#82D9C9

t3_2((t3)) --"Default " --> t4_1((tn))

style t4_1 fill:#F28DA8,stroke:#F28DA8

t3_2((t3)) --> t4_2((tn))

style t4_2 fill:#82D9C9,stroke:#82D9C9

t4_2 --> contractEnd(Contract End)

style contractEnd fill:#82D9C9,stroke:#82D9C9

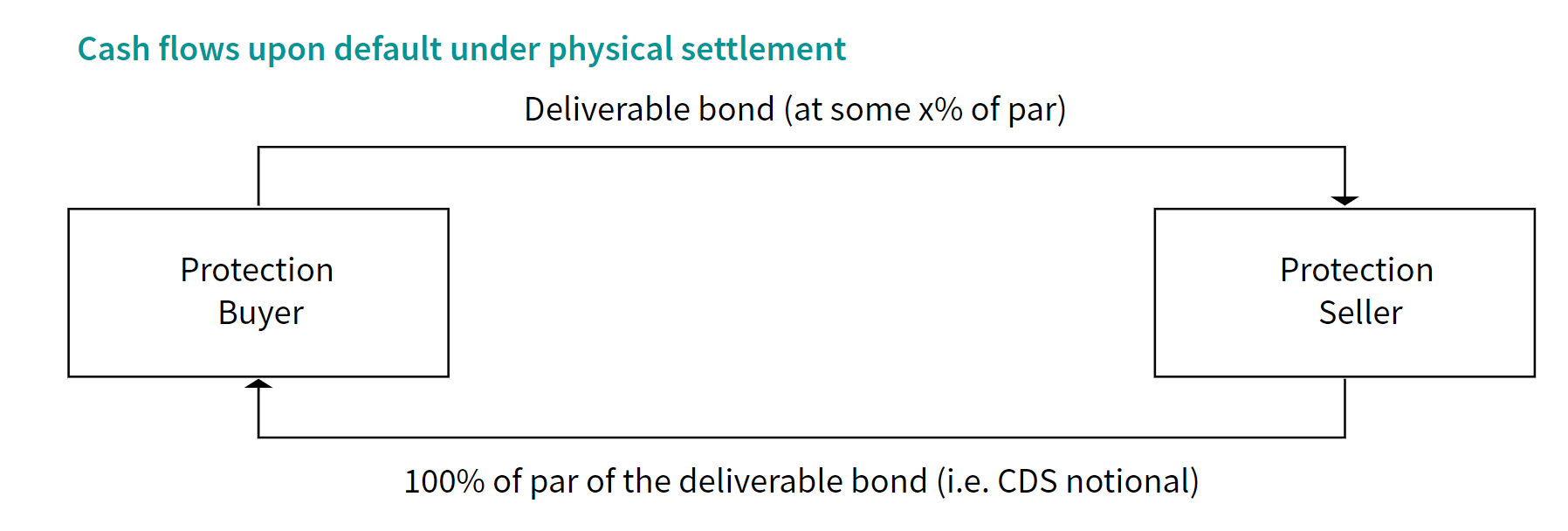

Physical settlement

The buyer sells impaired debt securities to the seller for par value.

i.e. In return, the seller takes delivery of a debt obligation of the reference entity.

where the projection buyer does not need to worry about the final recovery rates (RR)

:blue_book: For example, a hedge fund has bought 5 million worth of protection from a bank on a company’s senior debt. When default, the bank pays the hedge fund 5 million cash. The hedge fund must deliver 5 million face value of the company’s senior debt (typically bonds or loans, which are typically worth very little given that the company is in default).

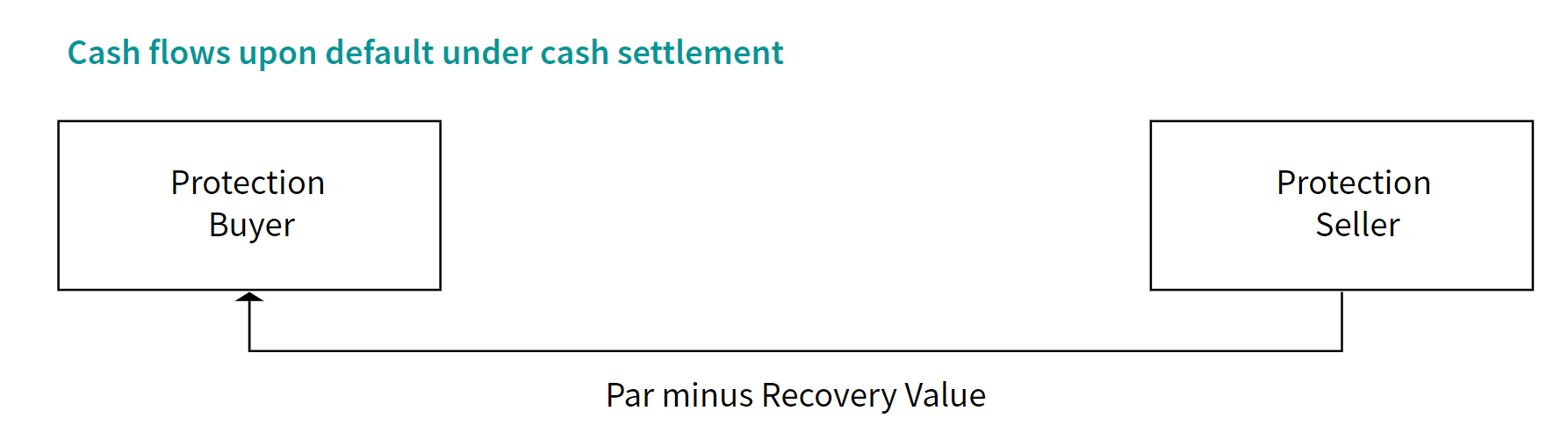

Cash settlement

Cash settlement: A payment is fixed or relative to the recovery rate.

i.e. The protection seller pays the buyer the difference between par value and the market price of a debt obligation of the reference entity.

:blue_book: For example, a hedge fund has bought 5 million worth of protection from a bank on a company’s senior debt. This company has now defaulted, and its senior bonds are now trading at 25 (i.e., 25 cents on the dollar) since the market believes that senior bondholders will receive 25% of the money they are owed once the company is wound up (all the defaulting company’s liquid assets are sold off). Therefore, the bank must pay the hedge fund.

5m * (100% − 25%) = 3.75 m

Auction

It is an industry-standard mechanism designed to ease the settlement of credit derivative trades following a credit event. The auction process determines the cash settlement price of a CDS, with the compensation received by the protection buyer based on the final agreed-upon auction price.

Motivation The notional value of protection contracts is often greater than the physical quantity of deliverable products. There are only a few reference obligations. Some contracts are cash-settled in a credit event auction.

The auction is designed to calculate the fair recovery rate.

$$

\text{Default Payments} = [(1-\mathrm{Recovery Rate}) \times \text { Par Value }]

$$

i.e. For example, following a default, the investor can

Option 1 – Sell the bonds to the protection seller for par value

Option 2 – Let the auction determine the fair recovery rate (like, say, 70%), so the investor would receive

$$

\text{Cash Settlement} = [(1-\mathrm{Recovery Rate 70%}) \times \text { Par Value }]

$$

The combination of bond sale (30%) and cash settlement (60%) generates a total value of par.

Compensation Payment

The compensation payment made by the protection seller to the protection buyer when a credit event happens

$$

\text { Compensation Payment }=\text { Notional Principal } \times \frac{\text { Par Value-Market Value after Credit Event }}{100}

$$